On March 12th this year, Roche announced a deal with Danish biotechnology company Zealand Pharma to co-commercialise Petrelintide, an anti-obesity drug. The deal resembles a minnow taking on a whale; a challenging feat, achieving commercial success amidst heavyweights Novo Nordsk and Eli Lilly in a crowded market.

This article seeks to understand whether co-commercialising Petrelintide is financially viable, and whether Roche paid a fair price for Zealand Pharma.

Introduction to Obesity Drug Market

The anti-obesity drug market has grown rapidly over the last three years. Largely driven by US consumption, drug makers are now positioning themselves on the international stage to continue on this growth trajectory. Germany, the UK, and Japan have become key regions for future growth.

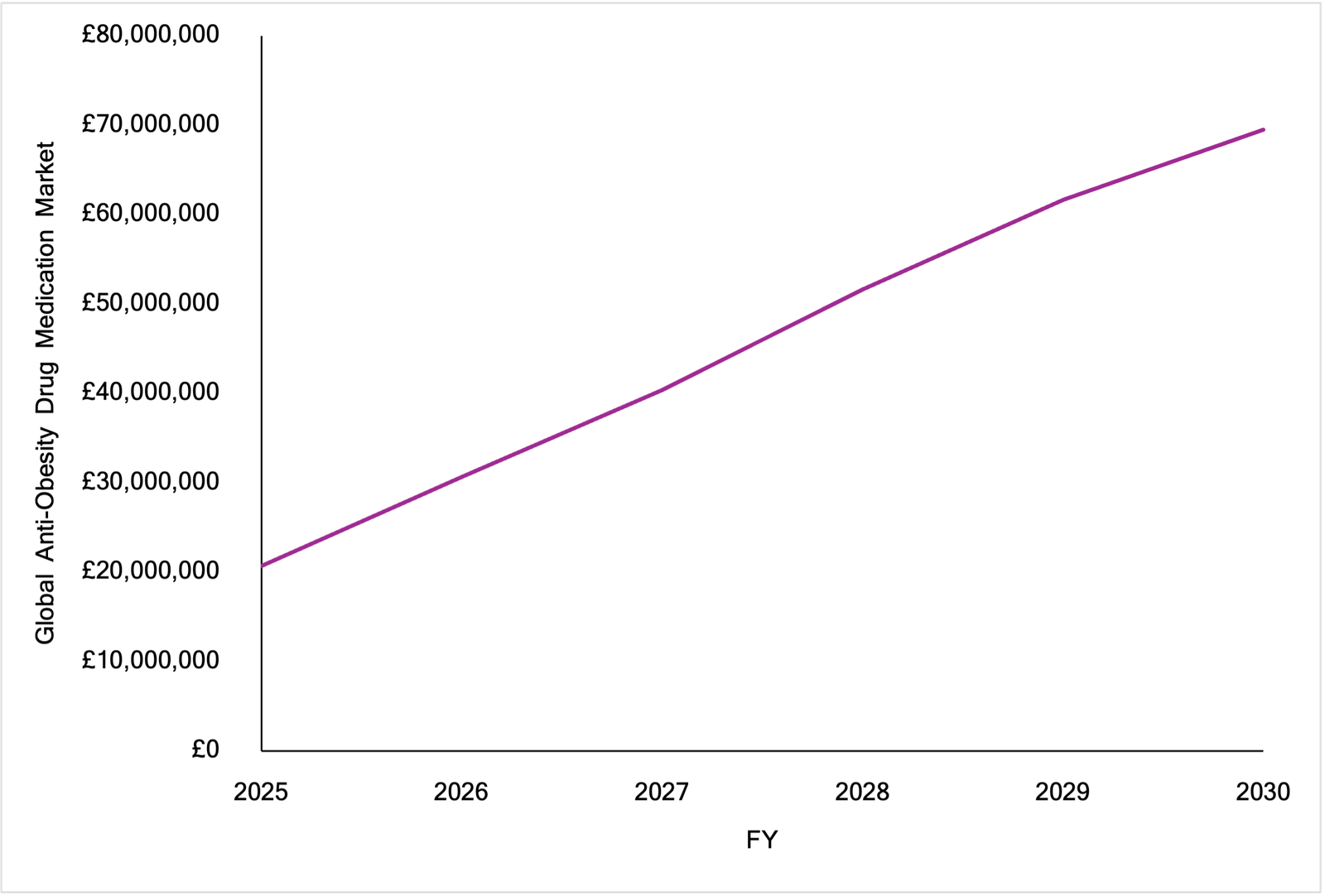

Market Forecasts by Goldman Sachs Research, May 2025

Within five years, the global anti-obesity drug medication market is expected to triple in size (in nominal terms), reaching £70 bn by 2030. This estimate is down £20 bn from previous forecasts earlier this year.

The market reflects a period of “watchful waiting”: overall confidence in anti-obesity drug market growth remains high. For behemoths of the anti-obesity drug market Novo Nordsk and Eli Lilly however, trade volatility and lower-than-expected trial results have lowered over-optimistic valuations slowly.

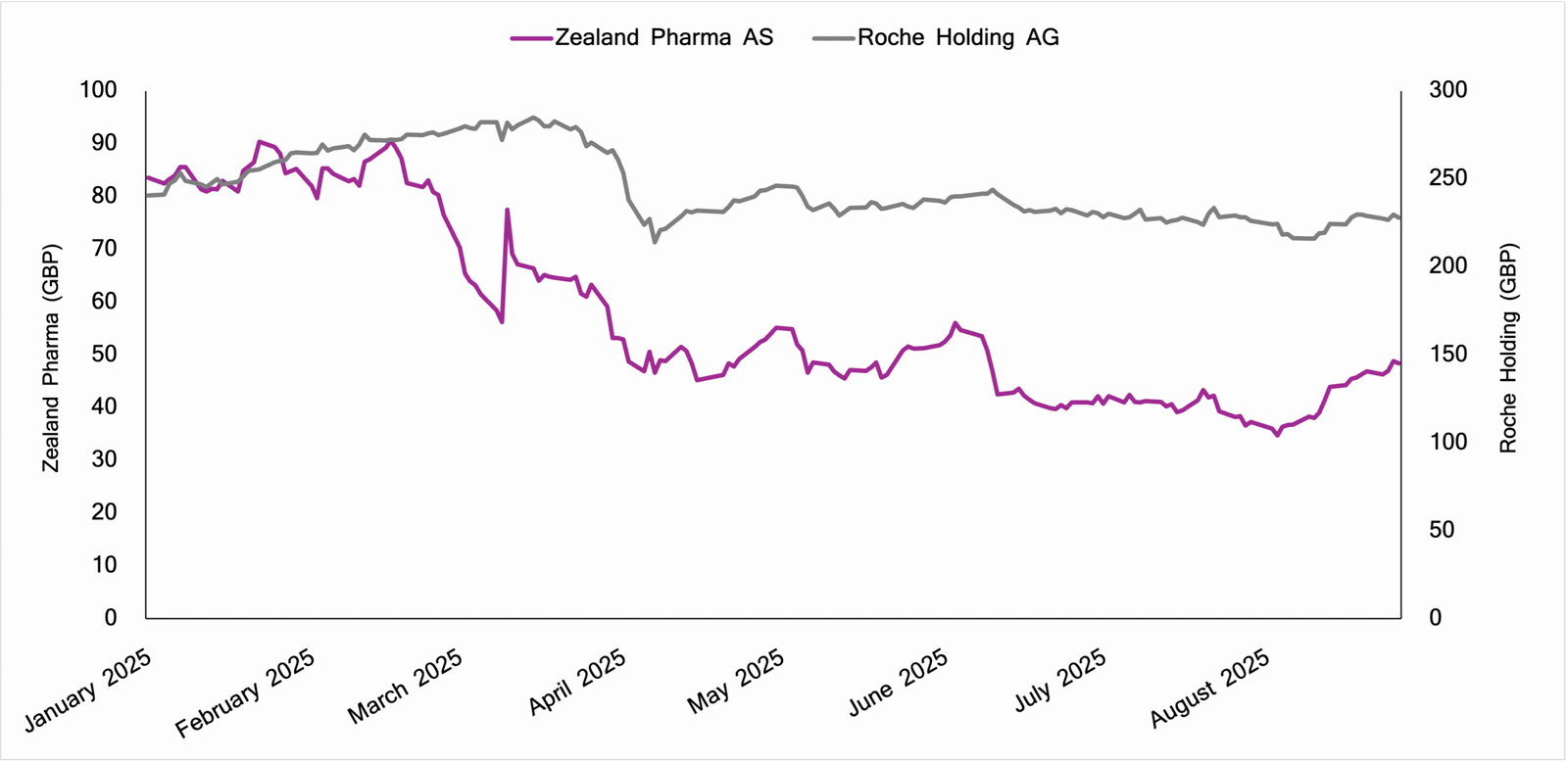

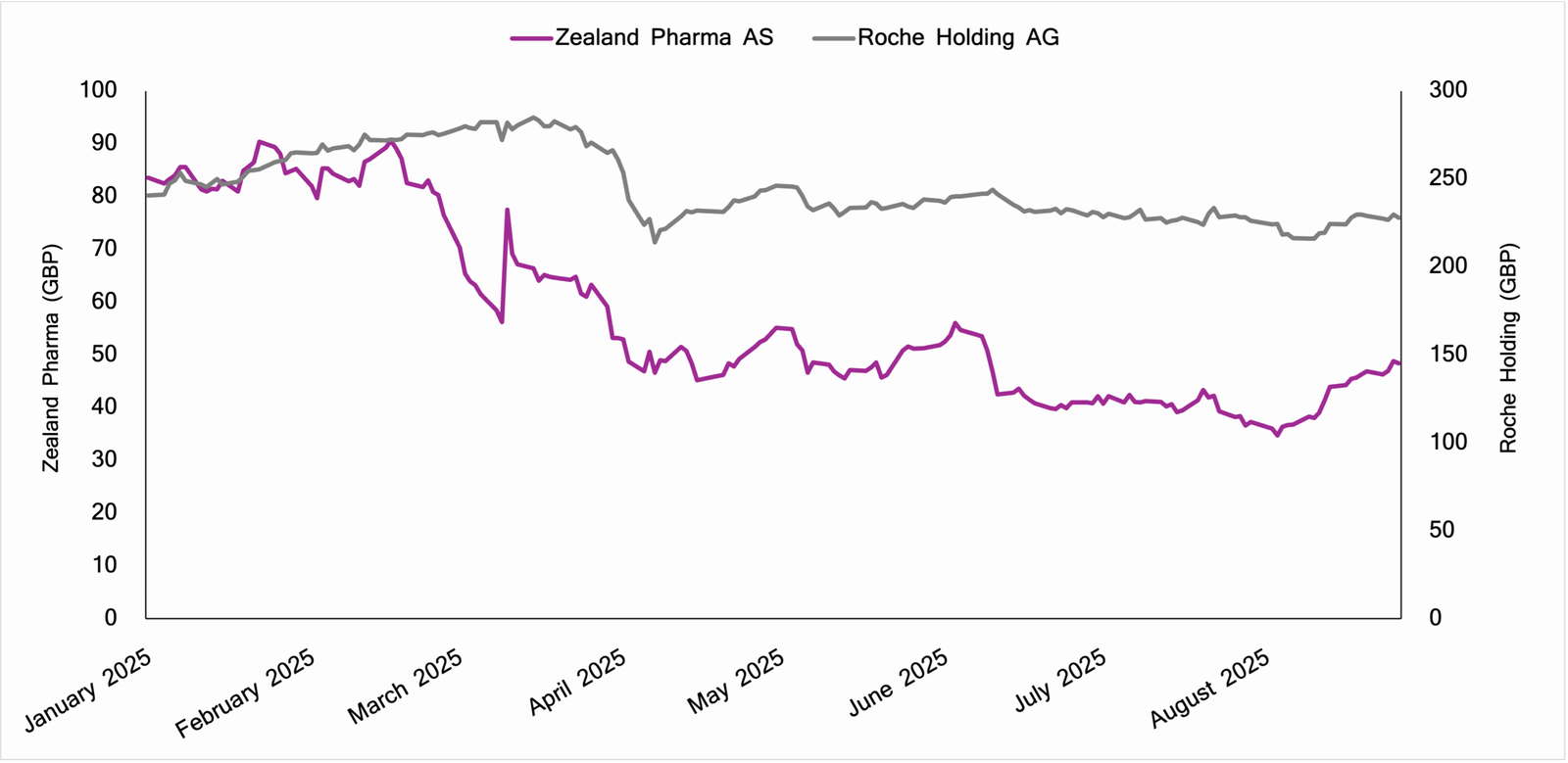

Stock Price Change, from 1st January 2025 to 31st August 2025

Novo Nordisk has struggled to shake negative sentiment following a series of disappointing trial results for its amylin analog candidate CagriSema, the active ingredient in Wegovy; fears of higher-than-15% tariffs on EU pharmaceutical imports to the US have spooked some investors, and; pressure from Trump on US drugmakers to increase European drug prices, keeping American prices low, has led to a month’s supply of Mounjaro increasing from £122 to £330. The combined effect has been sustained downward pressure on shares of Novo Nordisk and Eli Lilly.

Introduction to Zealand Pharma

Within the anti-obesity drug market operates a smaller biotechnology company, Zealand Pharma. The Danish company is responsible for producing innovative peptide-based treatments, and has been under the watchful eye of Roche – the Swiss pharmaceutical giant.

Stock Price Change, from 1st January 2025 to 31st August 2025

Like Eli Lilly and Novo Nordsk, Zealand Pharma has suffered this year from global trade volatility. Its share price has trailed downwards from £80 in March 2025 to £38 in August 2025. Roche, in contrast, has charted a steadier course.

Roche has been most interested in Zealand Pharma’s Petrelintide, an amylin analog that differs from GLP-1 anti-obesity drugs in its mechanism of action.

Amylin analogs mimic human amylin, a hormone co-secreted alongside insulin in the pancreas. Like Zepbound and Wegovy, amylin increases satiety, slows gastric emptying, and suppresses glucagon secretion. Unlike GLP-1s however, it can be combined with existing synthetic drugs, such as Roche’s lead incretin asset CT-388, to potentially achieve better efficacy. This is a focal point for Roche. Moreover, early clinical data points to comparable weight reduction between amylin analogs and GLP-1s, but with potentially superior tolerability and lean muscle preservation among the former – currently key sticking points for the industry.

March 2025 saw Roche enter into an exclusive collaboration and licensing agreement with Zealand Pharma. Under the terms, Zealand received upfront cash payments of £1.27 bn with potential milestone payments taking the total to up to £4.1 bn; dependent on Phase 3 trials and sales development. Currently, Zealand’s Petrelintide is being evaluated in a Phase 2 clinical programme.

This is the biggest-ever obesity drug deal. Is Roche overpaying?

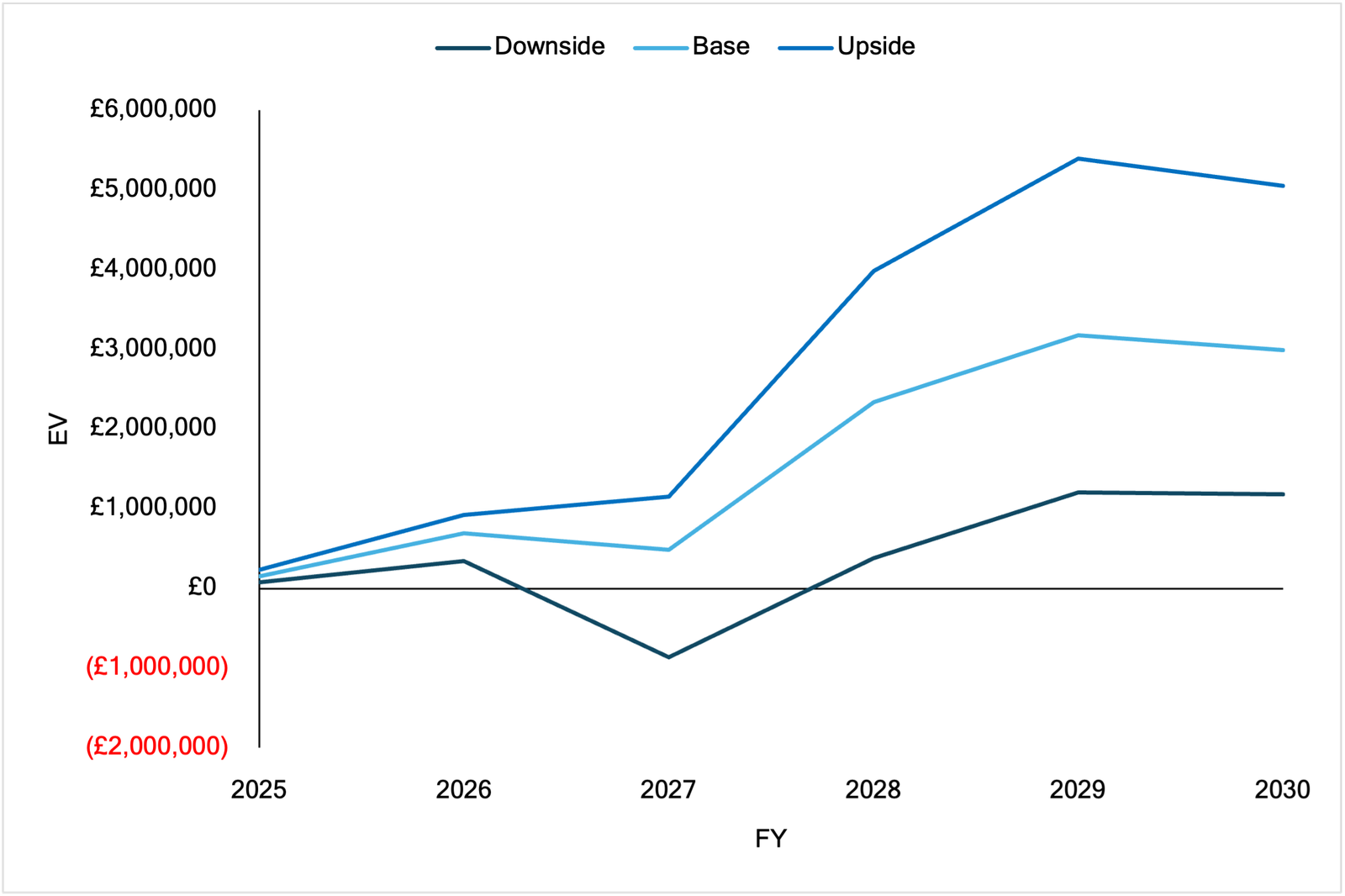

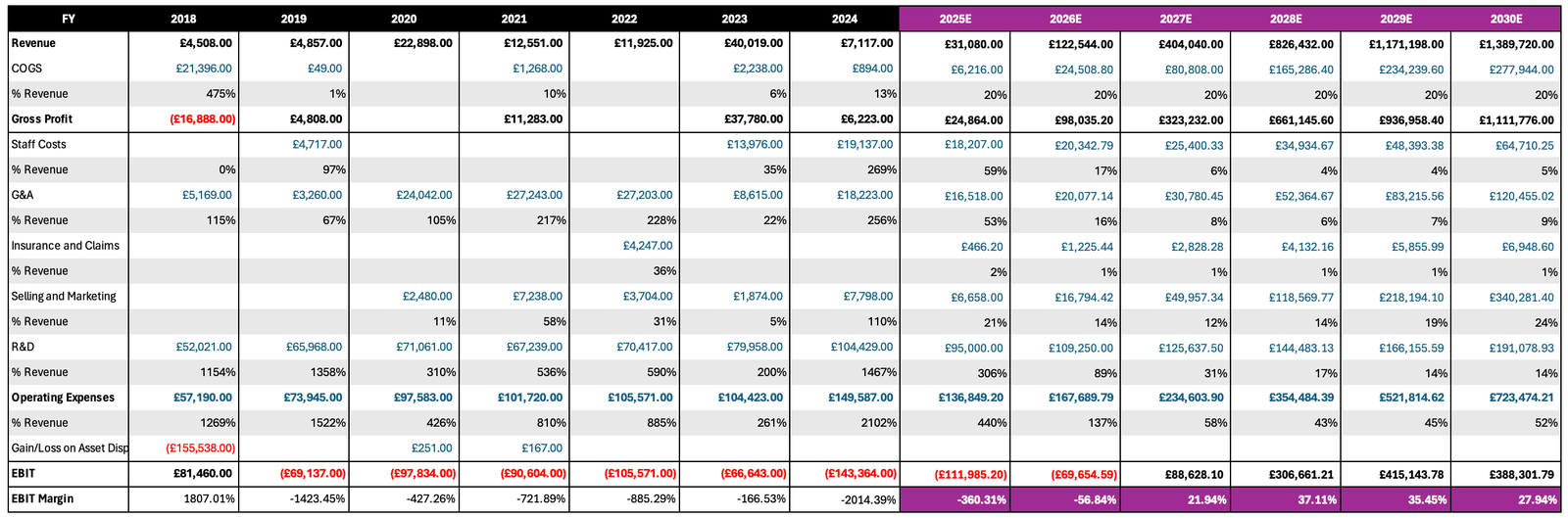

To answer this question, I forecast Zealand’s portfolio on a standalone basis. Roche’s deal economics can be mapped against these forecasts to assess whether Roche has overpaid, relative to the asset’s long-term potential.

Author Forecasts

In the bear case (1% share by 2030), EVs remain below Roche’s £1.27 bn entry point throughout the forecast period, implying value destruction. In the base case (1.5% share by 2030), EVs surpass £2.2-3.0bn from 2028 onwards, aligning with the structure of Roche’s milestone-linked payments. In the bull case (2% share by 2030), Zealand’s EV could reach £4-5 bn+ by 2029, making Roche’s upfront look attractive in hindsight.

Structurally, the milestone design mirrors these scenarios: Roche captures upside when targets are met but limits its exposure when they fall short.

If Zealand Pharma achieves 1.5-2% of the global anti-obesity market as revenue by 2030, the deal is commercially viable. Eli Lilly, for example, achieved more than this by 2022.

It may be a big ‘“if” however. Christoph Wirtz at Rothschild & Co Wealth Management agrees: “There are a lot of trials regarding obesity with different treatment technologies.” Eli Lilly and Novo Nordisk are in the “driver’s seat”, years ahead in expertise and manufacturing. “There is a long road ahead to make this deal successful [for Roche],” he said.

Appendix

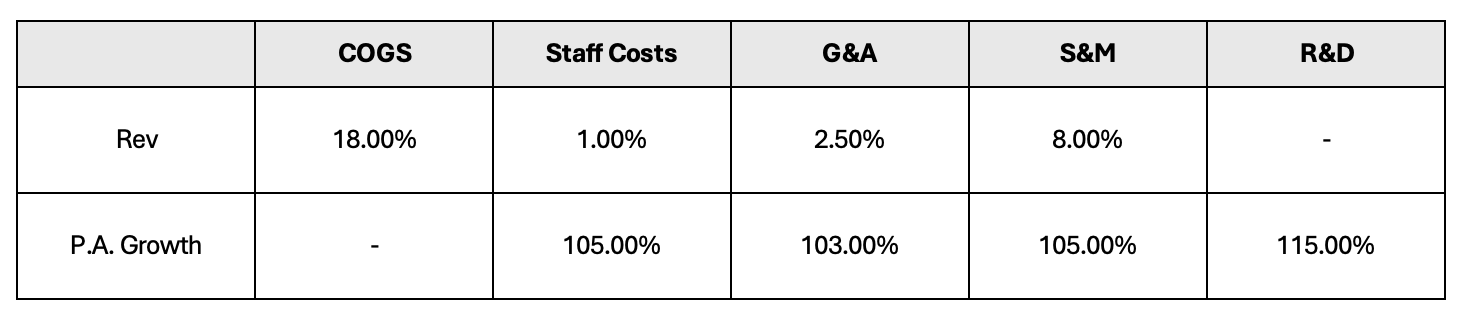

Operating expenses are forecasted using annual growth rates and shares of total revenue. These values, as pictured below, were closely mirrored with growth seen in historical Eli Lilly and Novo Nordsk OpEx values.

Sources

Financial Times — Eli Lilly’s weight-loss drug pricing in the UK

The Guardian — Eli Lilly to hike UK price of Mounjaro amid Trump pressure

Fortune Business Insights — Anti-obesity drugs market report

Goldman Sachs — The anti-obesity drug market may prove smaller than expected

Fortune Business Insights — Anti-obesity drugs market segmentation

Zealand Pharma — Pipeline: Petrelintide (amylin analogue)